The rising frequency and severity of claims prices past insurer expectations proceed to threaten insurance coverage protection and affordability. Triple-I’s newest Problem Temporary, Authorized System Abuse – State of the Danger describes how tendencies in claims litigation can drive social inflation, resulting in greater insurance coverage premiums for policyholders and losses for insurers.

Key Takeaways

- Insured losses proceed to exceed expectations and surpass inflation, notably impacting protection affordability and availability in Florida and Louisiana.

- In selling the time period “authorized system abuse”, Triple-I seeks to seize how litigation and associated systemic tendencies amplify social inflation.

- Progress has been made towards elevated consciousness in regards to the dangers of third-party litigation funding (TPLF), however extra work is required.

What we imply after we speak about authorized system abuse

Authorized system abuse happens when policyholders, plaintiff attorneys, or different third events use fraudulent or pointless ways in pursuing an insurance coverage declare payout, rising the time and value of settling insurance coverage claims. These actions can embrace unlawful maneuvers, corresponding to claims inflation and frivolous or outright fraudulent claims. Unscrupulous contractors, for instance, search to revenue from Project of Advantages (AOBs) by overstating restore prices after which submitting lawsuits in opposition to the insurer – generally even with out the home-owner’s data. Submitting a lawsuit to reap an outsized payout when it’s evident the claims course of will probably present a good, affordable, and well timed declare settlement may also be thought of authorized system abuse.

The newest temporary offers a round-up of a number of research Triple-I and different organizations performed on parts of those litigation tendencies. The report, “Affect of Rising Inflation on Private and Industrial Auto Legal responsibility Insurance coverage,” describes the $96 billion to $105 billion enhance in mixed declare payouts for U.S. private and industrial auto insurer legal responsibility. The Insurance coverage Analysis Council highlighted the dire lack of affordability for private auto and householders insurance coverage protection in Louisiana, together with the state’s exceptionally excessive declare litigation charges.

Readers will even discover an replace on the dialogue of authorized trade tendencies related to elevated claims litigation. The shortage of transparency round TPLF preparations and the worry of out of doors affect on instances are attracting the eye of legislators on the state and federal ranges. The temporary additionally describes how some legislation corporations might use TPLF assets to encourage massive windfall-seeking lawsuits as a substitute of speedy and truthful claims litigation. Analysis findings counsel that customers have turn into conscious of how ubiquitous lawyer adverts can affect the frequency of lawsuits, rising claims prices.

Florida: a case examine within the penalties of extreme litigation

Whereas a number of states, corresponding to California, Colorado, and Louisiana, are experiencing a drastic rise in the price of householders’ insurance coverage, this temporary discusses Florida. Property insurance coverage premiums there rank the best within the nation. A number of insurers going through insurmountable losses have stopped writing new insurance policies or left the state in the previous couple of years. In some areas, residents are leaving, too, due to skyrocketing premiums.

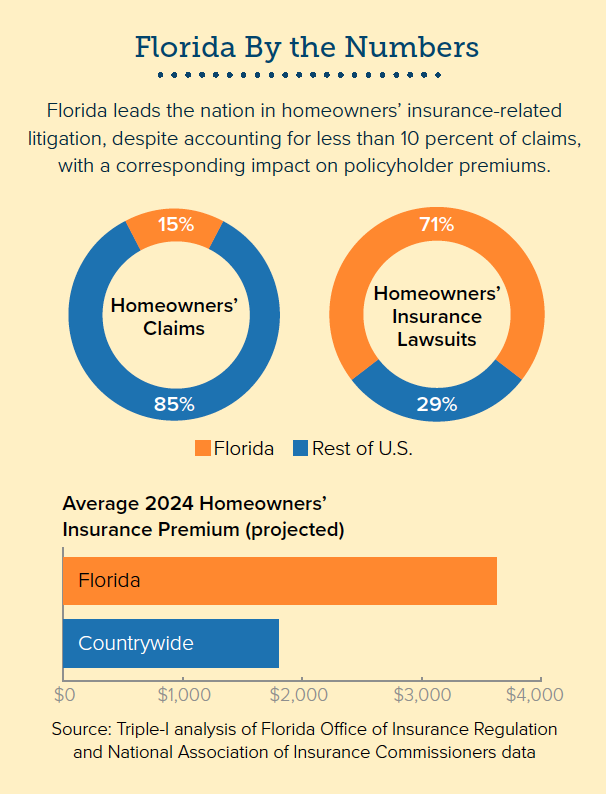

Extreme claims litigation isn’t a brand new difficulty for insurers, however it may possibly work with different parts to shift loss ratios and disrupt forecasts, rendering value administration more difficult. In Florida, components such because the rise in residence values and frequency of utmost climate occasions play a big position, together with the challenges householders face within the aftermath: hovering development prices, provide chain bottlenecks, and new constructing codes. Nonetheless, Florida additionally leads the nation in litigating property claims. Whereas 15 p.c of all householders claims within the nation originate within the state, Floridians file 71 p.c of householders insurance coverage lawsuits.

In Florida and elsewhere, rising time to settle a declare places a monetary pressure on insurers, which is handed on to policyholders within the type of greater premiums. Authorized system abuse actions are tough (if not not possible) to forecast and mitigate, hampering insurers’ potential to stay out there. Due to this fact, authorized system abuse could possibly be one of many greatest underlying drivers of social inflation. With out preventive measures, corresponding to coverage intervention and elevated policyholder consciousness, protection affordability and availability is in danger.

Triple-I stays dedicated to advancing the dialog and exploring actionable methods with all stakeholders. Study extra about authorized system abuse and its elements, corresponding to third-party litigation funding by following our weblog and testing our social inflation data hub.