GlobalData surveying signifies that many shoppers trying to change insurance coverage suppliers are literally struggling to search out higher offers regardless of rampant premium hikes in lots of private strains. The information that MoneySuperMarket introduced file annual income from its insurance coverage division in 2023, up 28% in 2022, exhibits the problem insurers face in competing on value in such a value-driven market. With premiums at file ranges and such a major proportion of shoppers trying to change (even when many can not), the aggregator has seen such spectacular outcomes by means of increased commissions and improved conversion charges.

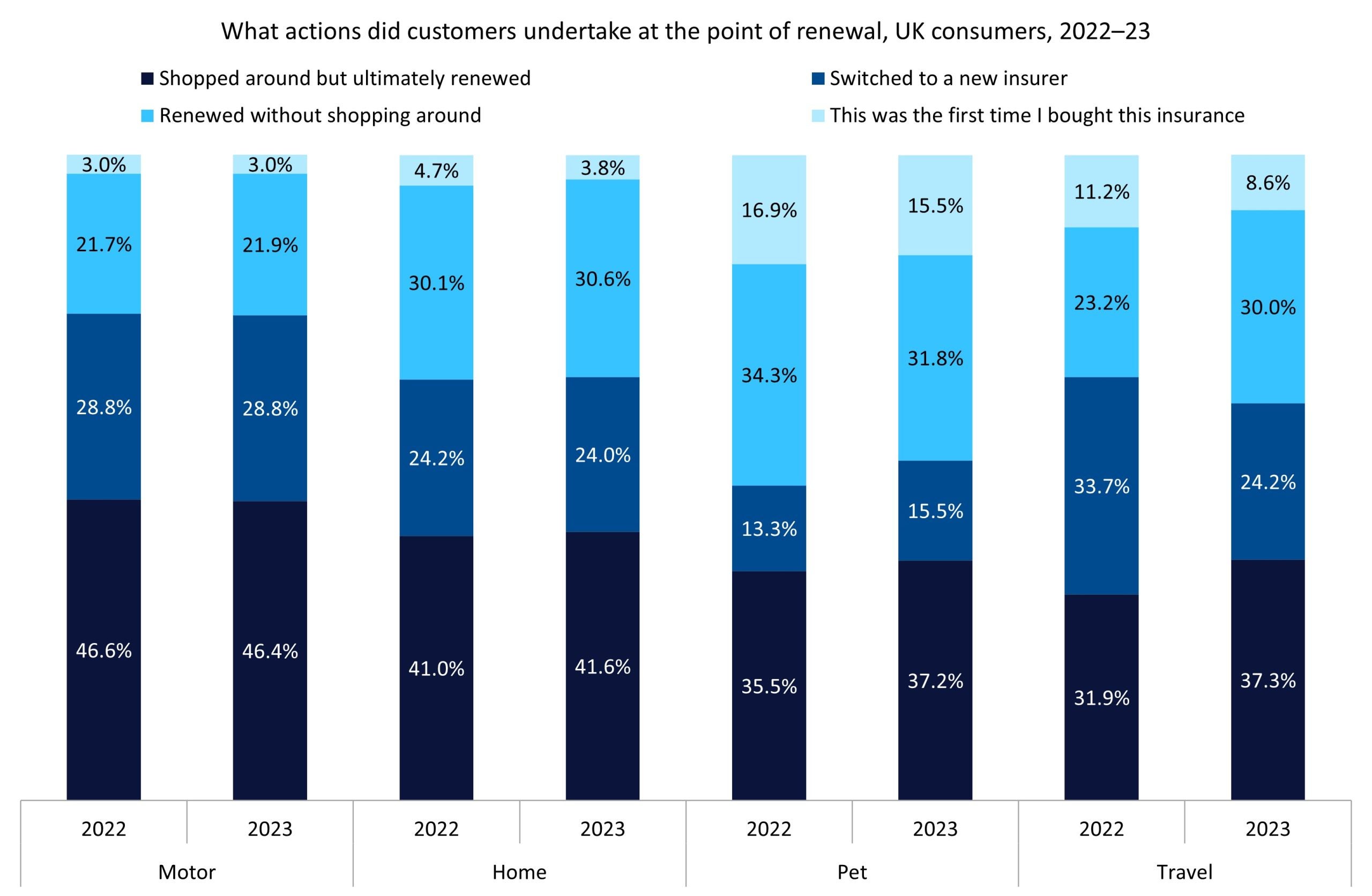

Value comparability web sites (PCWs) are uniquely positioned to reap the benefits of spiralling insurance coverage premiums within the post-pandemic world. In response to GlobalData’s 2023 UK Insurance coverage Shopper Survey, greater than 50% of UK insurance coverage prospects shopped round earlier than both switching or renewing with their insurer. Premiums within the motor and residential strains have risen considerably up to now two years. Information from the Affiliation of British Insurers (ABI) signifies the typical premium elevated by 33.5% between This autumn 2022 and This autumn 2023. For mixed, buildings-only, and contents-only insurance policies, these will increase have been 19.1%, 21.9%, and 12%, respectively.

Given these hefty value rises (along with the myriad of different further prices handed on to shoppers up to now few years), it’s no shock that so many people are in search of higher offers on their insurance coverage. Within the motor line, 75.2% of shoppers shopped round earlier than renewing or switching their coverage. Simply over one-third of this group discovered a less expensive supplier and switched. These figures are largely just like 2022, suggesting a secure and aggressive market as many shoppers have been unable to search out higher offers even when actively looking. Comparable findings have been seen within the residence line, with 65.6% of shoppers procuring round in 2023; once more, simply over one-third of this cohort have been capable of finding an alternate and change.

Sturdy competitors throughout private strains, accompanied by spiralling prices (in each claims and working bills), has put large stress on insurers. RSA’s exit from UK private strains exhibits that even the biggest gamers are struggling to maintain up with these prices. In 2022, RSA was the second-largest residence insurance coverage supplier, with an 11.3% market share as per GlobalData’s UK Prime 25 Normal Insurance coverage Competitor Analytics. Insurance coverage has at all times been a value-driven market—greater than 60% of all switchers did so as a consequence of a decrease premium from their new insurer—and the cost-of-living disaster has pushed much more shoppers to squeeze the utmost worth from their merchandise. The development of financially constrained shoppers in search of higher offers on their insurance coverage (or cancelling altogether) will certainly proceed in 2024. Insurers will battle to repeatedly move rising prices on to shoppers and so should discover a means of minimizing claims and working prices. In any other case, a repeat of 2023—by which the one winners appear to have been PCWs—seems a certainty.

Entry essentially the most complete Firm Profiles

available on the market, powered by GlobalData. Save hours of analysis. Acquire aggressive edge.

Firm Profile – free

pattern

Thanks!

Your obtain e-mail will arrive shortly

We’re assured concerning the

distinctive

high quality of our Firm Profiles. Nonetheless, we wish you to take advantage of

useful

determination for your corporation, so we provide a free pattern that you may obtain by

submitting the beneath type

By GlobalData