Is long-term care insurance coverage price it? Who would probably profit from this kind of protection? What’s the coverage’s largest disadvantage? Discover the solutions right here

Senior-age Individuals have round 70% likelihood of needing long-term care assist or companies, in line with the most recent authorities estimates. Entry to those companies, nevertheless, comes at a steep value. With out the fitting protection, the excessive price can simply deplete your retirement funds.

Sadly, medical insurance doesn’t cowl some of these bills. To be protected, you will want to get long-term care insurance coverage.

On this shopper schooling article, Insurance coverage Enterprise solutions the query, “Is long-term care insurance coverage price it?” We’ll focus on the coverage’s execs and cons, how a lot premiums price, and the fitting age to get protection.

When you’re planning on your personal care or serving to an older cherished one, you’ve come to the fitting place. Discover out the solutions to essentially the most urgent questions on long-term care insurance coverage on this information.

There’s a robust chance that you will want long-term care companies when you flip 65 primarily based on the figures gathered by the Administration for Neighborhood Dwelling (ACL).

The company’s information additionally reveals that males would require long-term care assist for a mean of two.2 years, whereas ladies shall be needing it for 3.7 years. No matter gender, 1 / 4 of American seniors might require care companies for no less than 5 years.

Common price of care assist and companies within the US

|

AVERAGE COST OF LONG-TERM CARE SERVICES

|

||

|

Sort of service

|

Common month-to-month fee

|

Common yearly fee

|

|

Homemaker companies

|

$5,720

(44 hours per week)

|

$68,640

|

|

House well being support

|

$6,292

(44 hours per week)

|

$75,504

|

|

Grownup day well being care

|

$2,058

|

$24,696

|

|

Assisted residing facility

|

$5,350

|

$64,200

|

|

Nursing house facility, semi-private room

|

$8,669

|

$104,028

|

|

Nursing house facility, personal room

|

$9,733

|

$116,796

|

Supply: Genworth, Value of Care Survey 2023

Given the steep prices, long-term care companies can eat into your retirement financial savings in a short time. Buying long-term care protection will help to handle this.

You may as well get help by means of Medicaid, however there are particular restrictions. One, your choices shall be restricted to nursing properties that settle for funds from the government-sponsored program. Additionally, you will have to exhaust most of your financial savings to get protection. Regardless of this, Medicaid received’t pay for all of your assisted residing bills.

The tables under include information from the American Affiliation for Lengthy Time period Care Insurance coverage’s (AALTCI) newest value index. The figures present how a lot you’ll be able to count on to pay in annual premiums for a long-term care insurance coverage coverage price $165,000.

The prices are categorized by age, gender, and marital standing. The information additionally consists of the price of insurance policies with inflation progress provisions.

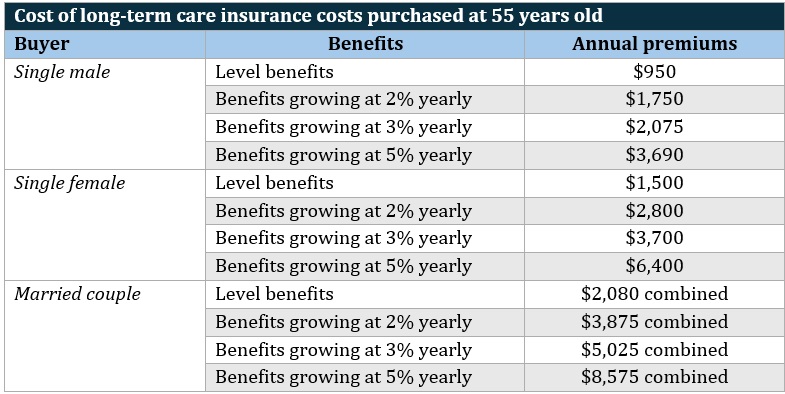

Is long-term care insurance coverage price it – price for insurance policies bought at 55 years previous

AALTCI’s value index reveals that the worth of the coverage can develop to $298,900 as soon as the holder reaches 85 years previous for plans with a 2% inflation progress provision. For these with 3% provisions, the worth can prime $400,500 and $679,100 for insurance policies with a 5% inflation profit.

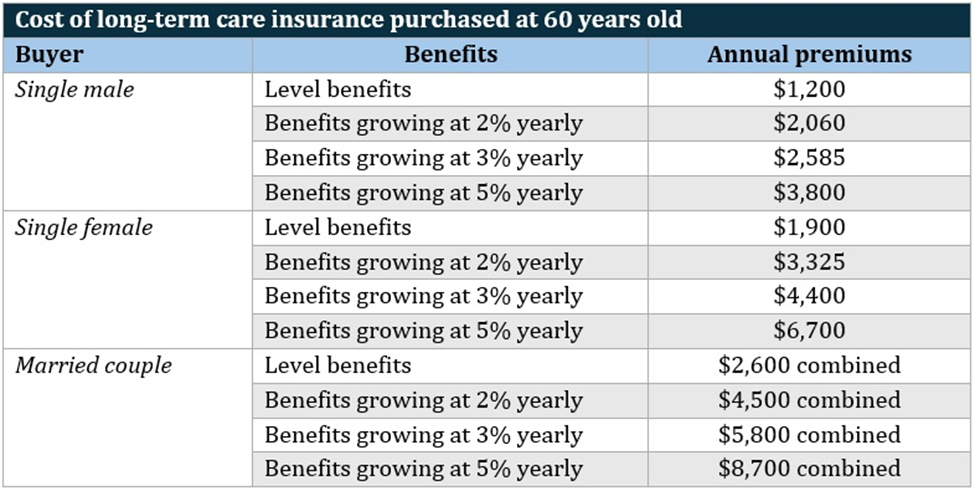

Is long-term care insurance coverage price it – price for insurance policies bought at 60 years previous

Lengthy-term care insurance coverage protection could be price $270,700 on the policyholder’s eighty fifth birthday if the plan has a 2% inflation progress provision. The worth will increase to $345,500 and $588,750 for insurance policies with 3% and 5% inflation advantages.

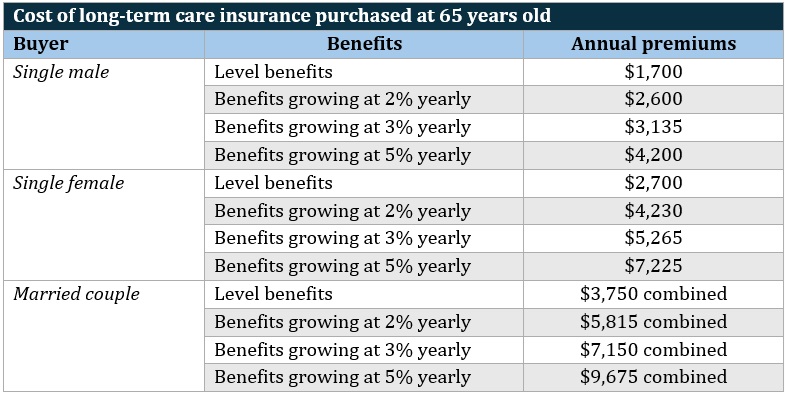

Is long-term care insurance coverage price it – price for insurance policies bought at 65 years previous

The worth of long-term care insurance policy with 2% inflation progress provisions can rise to $245,000 after the policyholder turns 85. The insurance policies could be price $298,500 and $437,800 if they’ve respective inflation advantages of three% and 5%.

The figures above are for “Choose” long-term care insurance coverage insurance policies. These are costlier than “Most well-liked” plans, in line with the AALTCI. The business non-profit provides that the charges are for seniors residing in Illinois. Your premiums could be greater or decrease, relying on various factors, together with the place you reside.

Every state has its personal standards on who can qualify for long-term care insurance coverage advantages. Most would require you to get certification that you would be able to not carry out no less than two of the six actions for day by day residing (ADL). These are:

- consuming: feeding your self

- bathing: getting out and in of the lavatory to scrub your self

- dressing: placing on or taking off your garments

- continence: controlling urinary and bowel actions

- toileting: getting on and off the bathroom

- transferring: getting out and in of a mattress or a chair

These affected by a debilitating situation could also be eligible for protection. These situations might embody:

- Alzheimer’s illness

- schizophrenia

- dementia

- a number of sclerosis

- Parkinson’s illness

- Lou Gehrig’s illness

One of many largest myths about long-term care insurance coverage is that it’s designed for seniors who want help due to age-related impairments.

Krystie Dascoli, voluntary advantages follow chief at Marsh McLennan Company, notes that anybody can develop situations or get into accidents that may affect their long-term well being. This highlights the necessity for long-term care insurance coverage throughout completely different age teams.

“Lengthy-term care can occur at any time in somebody’s life, not simply on account of previous age or power sickness,” she explains. “This can be a nice program to enhance different monetary wellness applications equivalent to time period life and incapacity insurance coverage.”

Some business specialists suggest taking out long-term care insurance coverage when you’re younger. This will help you entry decrease premiums, though you will want to pay for the coverage longer.

Dascoli suggests getting protection when you’re nonetheless gainfully employed.

“Charges will go up considerably with age, so shopping for a long-term care coverage early within the working years is right,” she says.

When you’re already 65 years previous however haven’t bought long-term care insurance coverage, taking out protection ought to nonetheless be a consideration, she provides.

“A giant mistake we see people make is ready till after retirement to buy long-term care insurance coverage. By buying long-term care plans throughout their working years and thru their employer, people could have the chance to purchase this insurance coverage with out answering medical questions and often have entry to greater face quantities. That is particularly necessary for anybody with pre-existing medical situations.”

The American Affiliation of Retired Individuals (AARP) says your early to mid-60s is the “candy spot” for those who’re single. For married {couples}, the most effective time to get long-term care insurance coverage is at 55 years previous.

The group provides that premiums could also be greater while you purchase protection at this age vary than it could have been in your late 40s to early 50s. The profit is you’ll be paying much less premiums general till you attain 80.

Lengthy-term care insurance coverage is commonly an costly type of protection. So, it might not all the time be accessible to low-income people.

One of many largest drawbacks of getting long-term care insurance coverage is the danger of shedding all of the premiums you will have paid over time. If you find yourself not needing long-term care companies, you received’t be eligible for protection. This implies the cash you’ve spent for protection goes down the drain.

“A person who purchases a standalone long-term care coverage has a 50/50 likelihood of utilizing it,” Dascoli notes. “Standalone or conventional long-term care insurance coverage is a ‘use it or lose it’ sort of coverage. An insured may maintain on to this kind of coverage for a few years and by no means use it.”

She recommends shopping for an alternate type of protection as an alternative, known as hybrid life insurance coverage.

“This can be a multi-use coverage that not solely pays a dying profit, but in addition pays out when the person is identified with a terminal sickness or wants long-term care,” she explains. “We promote the hybrid insurance policies extra as a result of, sooner or later, the person will use it and it additionally builds money worth.

“The one actual draw back to both of those insurance policies is that premiums could be steep, particularly the older a person will get. It is very important buy a hybrid coverage at a younger age to supply essentially the most monetary safety long-term.”

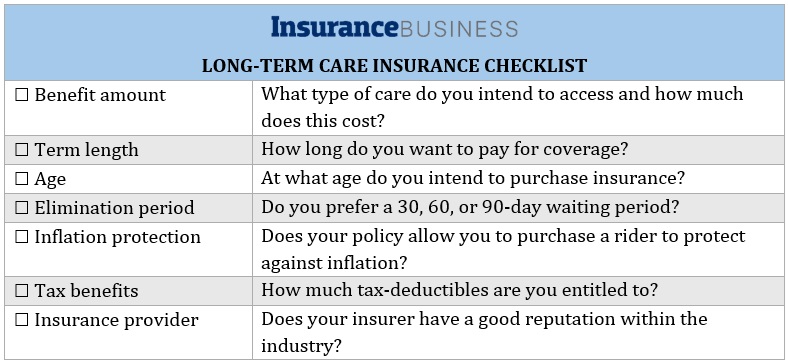

To search out the long-term care insurance coverage coverage that matches your potential care wants, there are a number of elements it is advisable to think about:

Profit quantity

Lengthy-term care insurance coverage prices fluctuate relying on the standard of care companies and the place you intend to entry them. Care companies from a personal nursing facility, for instance, price greater than these for at-home care. Take into account the kind of care you count on to obtain and the way a lot it will price you.

Time period size

Time period lengths vary from two years to a lifetime. Your medical historical past is a significant figuring out issue for the way lengthy you could pay for the coverage. If your loved ones has a historical past of a debilitating sickness, it might be higher to decide on an extended profit interval.

Age

Shopping for long-term care insurance coverage at a youthful age will help cut back your yearly premiums, though you will want to make funds longer. Getting protection nearer to senior age can increase your annual prices, however with a shorter fee interval, it’s possible you’ll find yourself paying much less premiums general.

Ready interval

Insurers impose ready durations of 30, 60, or 90 days earlier than you can begin receiving advantages and reimbursements. This implies you will want to cowl for medical bills out of pocket for a sure timeframe. When you select an extended ready interval, you might be able to entry decrease premiums.

Inflation advantages

Inflation may cause medical prices to soar. This is the reason long-term care insurance coverage suppliers supply add-ons to guard towards this. This function will increase your day by day advantages to meet up with inflation however pushes up your premiums.

Tax advantages

Many insurers supply tax-qualified insurance policies. These include tax-free advantages and deductible premiums. The deduction quantity varies relying on the taxpayer’s age.

Insurer status

It’s necessary that you just follow due diligence when selecting an insurance coverage firm. Go together with an insurer that’s each financially steady and dedicated to offering purchasers with the very best care.

Right here’s a guidelines of what it is advisable to think about in selecting a long-term care insurance coverage that’s price it. You’ll be able to obtain and print the record for straightforward reference.

Is long-term care insurance coverage price it – coverage guidelines

You may as well head to our Greatest in Insurance coverage Particular Studies web page if you wish to discover a long-term care insurance coverage supplier that provides top-notch protection. The businesses featured in our particular studies have been nominated by their friends. They’ve additionally been vetted by our panel of specialists as reliable and revered market leaders. By partnering with these insurers, you’ll be able to make certain that your wants are effectively taken care of.

Is long-term care insurance coverage price it? When do you suppose is the fitting time to purchase protection? Tell us within the feedback.

Sustain with the most recent information and occasions

Be part of our mailing record, it’s free!