Choose your strain. In case your group needed to have a ache level, would you relatively have…

- Increased than regular common declare prices because of inflation and provide chain challenges?

- Rising expense construction because of rising expertise and core working system prices?

- Larger threat and underwriting losses as a direct results of unpredictable climate?

- Lack of information insights to enhance A. B. or C.?

Sadly for in the present day’s P&C insurers, the enterprise local weather has been chosen for them.

E. All the Above

P&C insurers are in a very tight spot. Title a strain and it’s taking place proper now to them. It might be non permanent. It will not be as unhealthy because it has ever been. However, it’s difficult sufficient that insurers should take steps to alleviate their pains and pressures and create alternatives.

In accordance with A.M. Greatest’s Q1-2023 report, the P&C mixed ratio worsened by 6.1 share factors to 102.0 in Q123 (when in comparison with the prior 12 months’s quarter.)[i] In 2022, The US property-casualty insurance coverage market skilled a $26.5 billion web underwriting loss, a decline of $21.5 billion from the prior 12 months’s underwriting loss, in accordance with A.M. Greatest.

Whereas environmental climate and pure disasters equivalent to wildfires, hurricanes, or different catastrophic occasions, are prime of thoughts, there’s a rising set of recent dangers together with societal and technological. And most lately we’ve got as soon as once more seen the affect of monetary threat with the latest failure of Silicon Valley Financial institution and the continuing fallout. As famous in an article in Insurance coverage Journal, the failure was a scarcity of efficient threat administration.

All of those developments point out P&C insurers should rethink threat administration methods from merchandise and pricing to claims and prevention. As an alternative of taking part in protection, insurers should go on offense. However that requires a unique operational and know-how technique and method.

At a latest Majesco and Capgemini roundtable, trade specialists mentioned the altering threat surroundings and which adjustments insurers might make to show E. All the Above into Not one of the Above. You’ll be able to learn extra about this in our standpoint report, The Altering World of Threat: Insurers and Brokers on the Middle of Threat. In in the present day’s weblog, we glance particularly at pressures that may be mitigated by means of improved applied sciences.

A correct evaluation of threat contains…

Up to now, we might have checked out a particular coverage threat for solutions to loss likelihood and profitability. At this time’s threat requires a wider lens, together with:

- How a coverage threat impacts the general portfolio threat (and portfolio profitability).

- What different layers of threat ought to be thought-about together with environmental, societal, and technological dangers?

- How can loss management be used to evaluate each threat cost-effectively to handle the portfolio, reinsurance wants, and assist clients mitigate threat?

- How does customized knowledge shift underwriting and threat?

- How do insurers higher perceive new dangers?

Digital Autos (EVs) make a great case research for a broad method to understanding threat.

- As EV utilization grows, we are actually seeing the affect on claims because of accidents. We now have a number of incidents involving EV fires. Responders don’t essentially know tips on how to put these fires out. There have been situations of automotive doorways being “too digital” to open. When batteries are punctured, new dangers seem.

- Restore prices of EVs are costly. One instance is Rivian R1T pickup truck, which was rear-ended by a Lexus in February 2023 at a stoplight in Columbus, Ohio. The harm was initially deemed comparatively minor, and the opposite driver’s insurer provided him $1,600. The precise price to repair the bumper at a enterprise licensed to restore Rivian autos — one among simply three in Ohio — was $42,000, roughly half the truck’s promoting value[DG1] .

- Due to the complexities of EVs, many are totaled as a result of alternative of the battery is tough or unattainable to do, rising the danger and price.

- Legal responsibility isn’t straightforward to type out, particularly when the “driver” will not be driving. Would it not be the proprietor? The auto producer? For insurers, it turns into attempting to unravel a Rubik’s dice of understanding all the probabilities and dimensions of threat.

House and Enterprise sensible property techniques have some comparable points, solely in some situations, new applied sciences could also be offering new protections.

- The sensible house has the flexibility to maintain monitor of dangers inside water provide, drainage, safety, and electrical techniques.

- As sensible house/sensible enterprise networks develop more and more tied to electrical techniques, some techniques could also be discovered to be outdated and overly-taxed — dangerous to policyholders and insurers.

- Are insurers ready to seize and assess the precise varieties of information that can defend policyholders, stop fires, water harm, and theft, and likewise cut back claims?

- Are insurers actively utilizing AI and knowledge personalization to speak shortly about coming dangers, equivalent to hail, fires, and storms?

The excellent news is that for essentially the most half, change and threat are accelerating change with insurers to adapt extra shortly operationally. It may be fearful in tempo, however definitely not within the alternative and outcomes that create new worth and advantages clients can count on:

- Larger protection — extra individuals and extra companies might discover themselves coated by means of extra related or newer choices and fewer steps to utilization, together with embedded protection, lowering the insurance coverage protection hole.

- Larger predictive safety — insurance coverage might enhance underwriting profitability, cut back its prices and clients’ prices by means of a dramatic uptick in loss management data-driven threat assessments for underwriting that additionally gives perception and proposals for threat avoidance or mitigation by means of proactive options.

- Larger effectivity and effectiveness — insurers are proper now grappling with operational challenges together with expertise shortages and tech debt that can give them the “excuse” to revamp their working fashions and introduce higher options and ecosystems to enhance operational outcomes.

- Larger resiliency — a rapidly-growing set of dangers is prone to spark off two ancillary developments: new product growth and higher threat information and response.

Mitigated threat is an improved expertise

Buyer expectations are yet one more very important strain level for insurers. These expectations are linked to the entire different pressures (e.g. — prevention improves buyer satisfaction AND earnings) however they deserve their very own consideration. Prospects live totally different existence and exhibit way more sturdy digital proficiency. They demand totally different experiences, and so they have totally different expectations about worth. In accordance with a latest AM Greatest innovation evaluation report, “the rise of digital platforms and ecosystems will make relationships with clients much more necessary.”

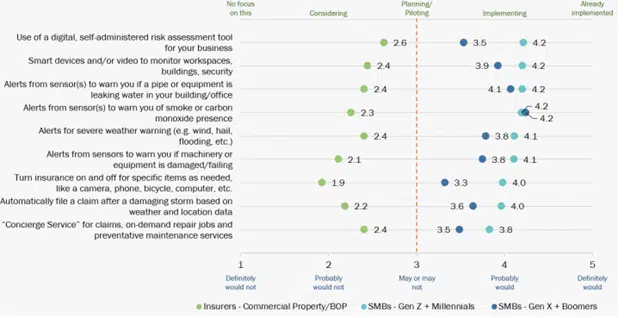

These altering expectations and wishes are making a disconnect between what they need and what insurers supply. The disconnect contains buyer altering priorities and merchandise wanted, demand for threat mitigation and avoidance, customized pricing and score based mostly on their particular threat profile and a necessity for value-added providers that stretch buyer worth and loyalty as seen in Determine 1.

Determine 1

The gaps between buyer expectations and what insurers are providing are practically twofold for each generational teams of SMBs and comparable for customers, based mostly on Majesco analysis! Prospects need and count on extra. To satisfy the elevated expectations, we have to establish priorities that can bridge the hole for insurers equivalent to digitalization, knowledge, and threat resilience — new methods of coping with each the brand new buyer and the brand new dangers we’re seeing in in the present day’s period.

Prospects need customized underwriting based mostly on their particular knowledge or steady evaluation of threat. The normal threat fashions or once-per-year, conventional method doesn’t work for the brand new dangers which can be offered. Knowledge and analytics and the way it impacts our threat perspective on a micro stage are extra consumable in methods that don’t pressure our know-how and our underwriting groups.

That is why there may be elevated curiosity in usage-based or telematics-based insurance coverage. In in the present day’s macroeconomic surroundings, clients try to handle their prices, together with insurance coverage premiums, therefore the elevated demand for telematics-based insurance coverage.

An ideal instance of the worth is within the latest earnings name from Progressive Insurance coverage Group and a view from Mike Zaremski, Sr. P&C insurance coverage fairness analysis analyst, and MD at BMO Capital Markets:

“Progressive is constructing upon its materials first-mover aggressive telematics benefit by providing a brand new crash-detection/security service to its clients. We estimate PGR’s aggressive benefit in telematics can be structural in that buyer adoption charges of telematics-based insurance policies through D-2-C distribution are multiples larger than through a dealer, which means PGR is constructing upon its aggressive benefit vs. its common peer every day (notice, most of its friends distribute through insurance coverage brokers).”

Worth-added providers contribute to threat resilience

We live in a world that has rising threat. Insurance coverage can now not be about simply underwriting after which ready for the declare to occur, however insurance coverage additionally should assist keep away from or decrease the danger, creating larger buyer worth.

Whereas most insurers are targeted on how they will higher assess threat, many extra are increasing to additionally give attention to the prevention of losses and creating threat resilience for purchasers. The adage of “management what you may management” is now entrance and middle for insurers as they have a look at new threat administration methods as an important part of their underwriting and customer support technique.

Main insurers are leveraging know-how equivalent to IoT gadgets, sensible watches, loss management assessments, and value-added providers to not solely assess and monitor threat however to proactively reply to it with mitigation providers and actions. From concierge providers to monitoring water hazards and the security of workers, to serving to to stay wholesome existence, main insurers are shifting to threat resilience methods that not solely drive higher enterprise outcomes but additionally produce nice buyer loyalty.

This creates threat resilience.

New applied sciences, paired with knowledge & analytics

One of many essential areas for insurers to fulfill the altering world of threat is with know-how and knowledge and analytics. They have to create a brand new basis that allows operational optimization and innovation by means of the alternative of legacy techniques, adoption of recent applied sciences, and embracing the strategic position of information and analytics.

Expertise is the essential basis to adapt, innovate and ship at velocity to execute on technique and market shifts. The rising significance and adoption of platform applied sciences, APIs, microservices, digital capabilities, new/non-traditional knowledge sources, and superior analytics capabilities – together with generative AI — are actually essential to development, profitability, buyer engagement, channel attain, and workforce change.

From the entrance workplace to the again workplace, SaaS platforms are reshaping the enterprise focus from coverage to buyer, from course of to expertise, from static to dynamic pricing, from point-in-time underwriting to steady underwriting, from a historic view of information to predictive and prescriptive knowledge, from conventional merchandise to new, modern merchandise, and a lot extra. Insurers’ potential to create an interconnected tech basis will ship each development and buyer relationship alternatives.

Superior analytics capabilities are poised to be a game-changer for insurance coverage. When new and real-time knowledge, superior analytics, AI and machine studying, and generative AI are successfully embedded into the operation and core techniques, insurers can have a big operational affect throughout your complete insurance coverage worth chain. Knowledge is changing into extra available and cheaper, changing into a commodity that permits it to unfold throughout your complete worth chain. And superior analytics with AI, ML, and NLP are rising as highly effective instruments to boost underwriting, establish and stop threat, and drive extra efficiencies, main to raised profitability and loss ratios.

Knowledge overload and diminishing velocity to insights

The swelling quantity of information is creating issue for underwriters to handle and use it successfully. The market is seeing large knowledge will increase in IoT machine knowledge, telematics knowledge, and risk-specific knowledge.

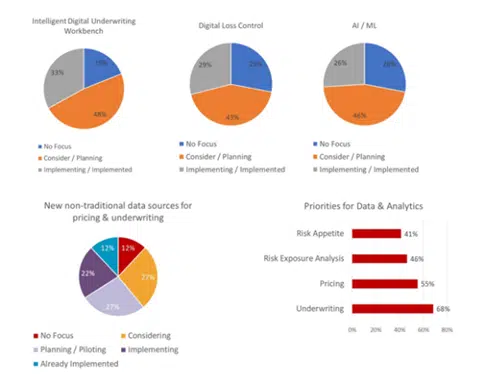

Underwriters and actuaries can’t validate and devise their understandings shortly sufficient, resulting in the need of automated strategies needing to be utilized to the info to attract perception to create higher and expedited enterprise choices. With the usage of extra correct knowledge, insurers can leverage predictive modeling to offer personalized protection and higher pricing. However it’s greater than anybody coverage. The mixture of clever underwriting, loss management and superior analytics like AI/ML are more and more essential to assess the particular threat, but additionally its affect by way of threat urge for food and threat publicity evaluation for the portfolio as seen in Determine 2.

Determine 2

Because the competitors tightens within the trade, each a part of the insurance coverage group should be dedicated to the usage of next-generation know-how and knowledge and analytics to face out from their rivals and to fulfill buyer expectations.

These caught on legacy core techniques are boxed in and are restricted of their potential. Transferring their enterprise to next-gen cloud platforms is essential, not only for single strains of enterprise, however for your complete enterprise to realize actual optimization and price discount. Extra importantly, it frees up assets to fund tomorrow’s enterprise.

Tomorrow’s enterprise should be digital, enabling the flexibility to quickly introduce new merchandise that seize new market segments, meet new dangers, buyer wants and expectations, and new distribution channels. It should embed insurance coverage into different services to make it simpler to know and buy.

For insurers, enterprise processes finally have to be considered in another way than in earlier occasions. It’s about being aggressive in prevention and giving your underwriters (and different workforce members) the instruments they should obtain one of the best outcomes. A renewed core and upgraded know-how will play a considerable position and assist insurers obtain a complicated loss management technique. Inside that know-how platform, insurers should additionally not be afraid to make the most of cloud capabilities that may assist enhance knowledge utilization and quicken the time that underwriters can produce protection choices.

Expertise is the essential basis for coping with the present and future pressures of a high-pressure P&C surroundings. It should assist insurers to adapt, innovate, and ship at velocity to execute on technique and market shifts. The rising significance and adoption of platform applied sciences, APIs, microservices, digital capabilities, new/non-traditional knowledge sources, and superior analytics capabilities are actually important to development, profitability, buyer engagement, channel attain, and workforce change.

For a deeper have a look at how rising ecosystem participation and efficient management are concerned in the identical risk-mitigation equation, you’ll want to obtain the Majesco/Capgemini standpoint report, The Altering World of Threat: Insurers and Brokers on the Middle of Threat.

At this time’s weblog is co-authored by Denise Garth, Chief Technique Officer at Majesco, and Kelly Reisling, Senior Director, Capgemini

[i] Willard, Jack, US P&C trade sees $8.2bn web underwriting loss in Q1: AM Greatest, June 16, 2023

[DG1]https://www.nytimes.com/2023/07/03/enterprise/car-repairs-electric-vehicles.html#:~:textual content=Datapercent20frompercent20Mitchellpercent20showspercent20that,requirepercent20workpercent20bypercent20specialistpercent20mechanics.