As one other tax submitting season involves a detailed, thousands and thousands of Individuals have lowered their taxable earnings via accounts that assist pay for medical prices. Underneath present legislation, individuals could make restricted pre-tax contributions to and withdrawals from a “well being financial savings account” (HSA), or let the cash respect in worth on a tax-free foundation. Along with being a frequent flyer in Republican well being plans, together with the latest Republican Examine Committee price range proposal, members of Congress have put forth bipartisan proposals to increase HSAs. However with the advantages of HSAs primarily accruing to more healthy and wealthier Individuals, increasing HSAs might exacerbate an already regressive tax break with out enhancing entry to protection or care.*

Background

HSAs are an account allowing people to save cash on a pre-tax foundation that may fund sure qualifying medical bills. Accounts supply a “triple” tax break—contributions, funding development, and withdrawals for eligible bills are all exempt from federal taxation. Annual contributions are capped—in 2024, people age 55 and beneath can contribute as much as $4,150 for self-only protection or $8,300 for household protection. Limits for these over 55 are increased. Employers can even contribute to employees’ HSAs.

HSA holders are required to pair the account with a high-deductible well being plan (HDHP). To qualify as an HDHP in 2024, a well being plan will need to have a deductible of not less than $1,600 for self-only protection and $3,200 for a household plan. In 2023, employees with HSA-qualifying HDHPs had common annual deductibles of $2,518 for self-only protection.

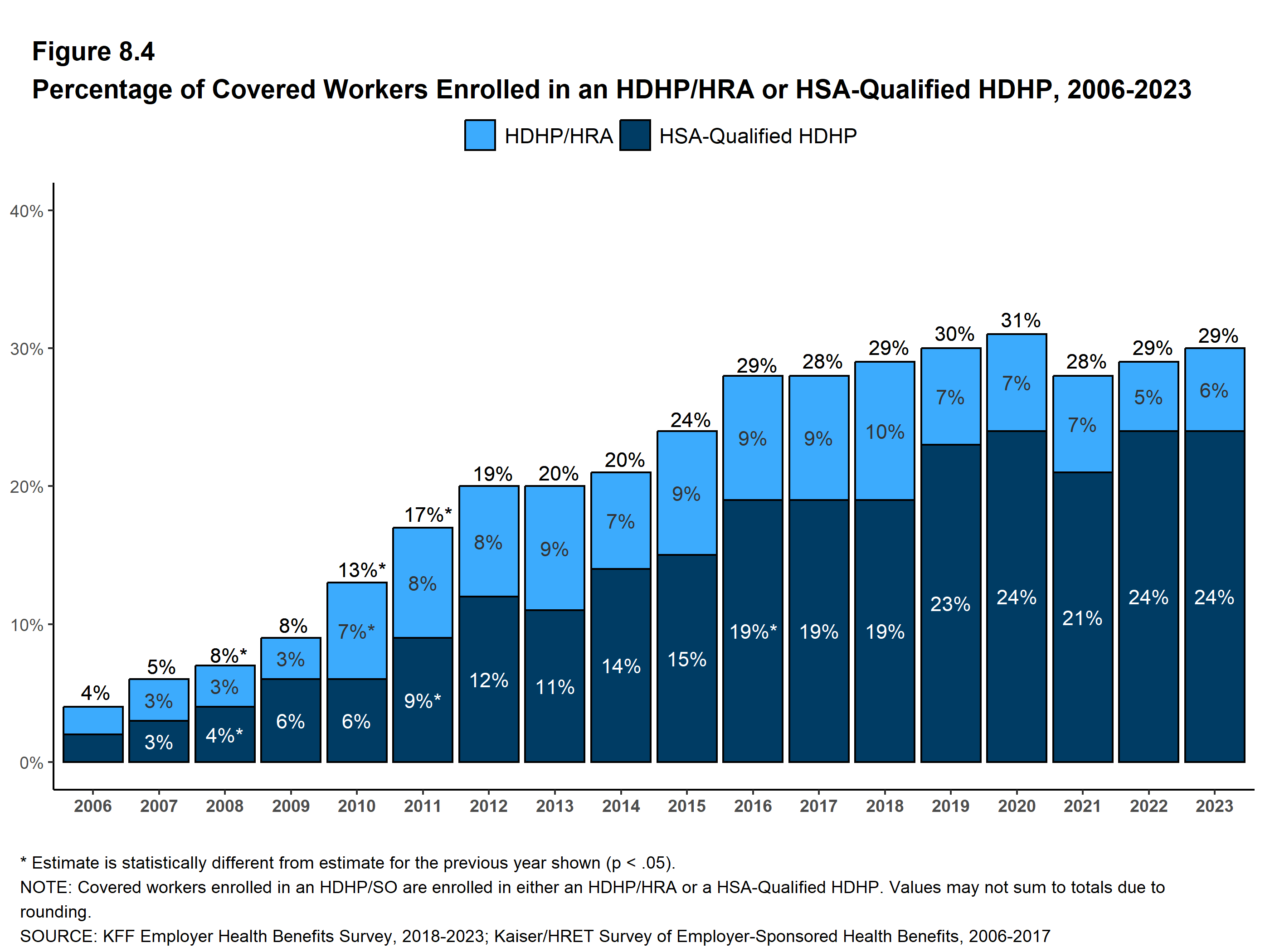

As of 2021, round one in six adults with personal medical insurance had an account, and in 2023, practically one in 4 employees with employer-sponsored medical insurance enrolled in an HSA-qualified HDHP (up from round one in 10 coated employees in 2013).

{kind=link}

In principle, this association offers enrollees “pores and skin within the sport,” encouraging them to buy round for decrease well being care costs and deterring utilization of low-value or pointless care. This dynamic is meant to scale back well being spending and promote an environment friendly well being care system. However embedded within the HDHP-HSA association is a regressive tax break and penalty for poor well being that creates limitations to take care of individuals who want it most.

The Proof is Clear: HSAs Assist the Wholesome and Rich on the Expense of the Sick and Poor

Earnings Disparities: A Tax Subsidy That Primarily Advantages Wealthier People

Most of the uninsured are in a decrease earnings bracket, however HSAs disproportionately profit the rich. HSAs present the best subsidy to individuals who want it the least; tax-free contributions are Most worthy to individuals within the highest tax brackets and least helpful to decrease earnings people. Unsurprisingly, high-income households are extra probably to make HSA contributions or obtain contributions from their employer, and have a tendency to contribute extra money to HSAs than decrease earnings account holders.

These earnings disparities are additional exacerbated by the position HSAs function a tax shelter and funding car. HSA contributions lower taxable earnings, and account holders can withdraw funds as reimbursement for earlier medical bills with out rising their taxable earnings, which might, for instance, enable them to keep away from coming into a better tax bracket. The accounts have additionally been touted as a tax-free funding possibility—an particularly engaging one for individuals who have already maximized contributions to different tax-advantaged accounts like an IRA.

Well being Disparities: Serving to the Wholesome and Penalizing the Sick

Along with earnings disparities, HSAs exacerbate well being disparities by rising prices for sick individuals whereas decreasing prices for more healthy people. Account holders are required to enroll in HDHPs, much less beneficiant well being plans with increased out-of-pocket prices. Whereas these plans typically include decrease premiums than merchandise with decrease deductibles, they will in the end be costlier for individuals with continual circumstances or different well being care wants. HDHPs are a a lot better deal for more healthy people who use much less care.

Accordingly, HDHPs paired with HSAs are typically extra engaging to the wholesome and rich. Utilizing the mixed tax break and decrease premiums related to HDHPs, HSA holders with substantial contributions and few well being care wants might put account funds in direction of issues like gymnasium memberships and meal kits, testing the bounds of what qualifies as a medical expense beneath present pointers.

Boundaries to Look after Low-Earnings Enrollees

Customers who can’t afford to sufficiently fund HSAs might face limitations to care. HDHPs impose excessive price sharing, a blunt instrument recognized to cut back utilization of each efficient care and ineffective care. These plans additionally cowl fewer pre-deductible providers—HDHPs can solely cowl preventive care pre-deductible (together with a restricted set of providers prescribed to deal with people with sure continual circumstances), subjecting enrollees to the total price of many objects and providers till their excessive deductible is met.

Due to these price limitations, enrollment in HDHPs is related with delayed and foregone care, notably amongst individuals with decrease incomes. Even use of preventive care—which should be coated with out cost-sharing by HDHPs—is decrease amongst HDHP enrollees, due not less than partly to enrollees’ lack of knowledge of free care and probably issues about the price of follow-up care.

Decrease earnings HDHP enrollees who find yourself needing well being providers might face further obstacles; episodes of care can depart them with huge payments, and personal insurance coverage enrollees with excessive deductibles are at a better danger of accruing medical debt.

This Regressive Tax Shelter Does Not Scale back HSA Holders’ Well being Spending

The first beneficiaries of HSAs might not be bending the well being care price curve as meant. Current proof suggests that folks enrolled in HDHPs with HSAs usually are not utilizing much less care in comparison with their counterparts who don’t maintain an HSA, and HDHP-HSA enrollees are reporting fewer monetary limitations to care than prior to now. Researchers have instructed that, as price sharing will increase throughout personal plans, higher-income Individuals receiving the extra “subsidy” from HSA tax advantages could also be utilizing it to acquire extra care.

Congressional Proposals to Broaden HSAs Would Exacerbate These Points

The present Congress has thought of a number of payments to increase HSAs, together with:

- Giving Employers a Cross on the Requirement to Provide Well being Insurance coverage: one other proposal wouldallow giant employers to fulfill the Inexpensive Care Act’s “employer mandate” by funding HSAs for workers to buy a Market plan, relieving them of their present responsibility to supply protection.

These proposals would predominantly assist higher-income and more healthy people, who profit extra from the tax benefits of HSAs and already face far fewer limitations to protection and care, by making HSAs extra profitable and versatile. Increasing HSAs would additionally additional incentivize more healthy and wealthier people to buy much less complete protection, exacerbating the prevailing dynamic that rewards people with fewer well being care wants and penalizes the sick.

Cash Subsidizing Rich Enrollees May As an alternative Fund a Main Protection Growth or Affordability Initiative

HSAs divert federal funds away from more practical protection expansions. The tax advantages of HSAs cut back federally taxable earnings and consequently federal income. Treasury estimates that tax exclusions for HSAs (and an identical medical financial savings account that preceded HSAs) will price the federal authorities practically $180 billion over the subsequent ten years. On high of this price, two payments marked up final yr by the Home Methods and Means Committee, together with proposed bipartisan laws, are anticipated to cut back income by a further $71 billion between 2024 and 2033 if enacted.

Federal expenditures related to HSAs and proposed expansions might as an alternative fund efforts to scale back the uninsured and enhance medical insurance affordability. The Heart on Finances and Coverage Priorities has identified that, over the subsequent ten years, the estimated price of closing the Medicaid hole is $200 billion, whereas completely extending the short-term Market subsidy enlargement beneath the American Rescue Plan Act, which helped produce file Market enrollment, would price $183 billion.

Takeaway

Entry to inexpensive, complete insurance coverage continues to be not a actuality for all Individuals. An ongoing problem to attaining universally inexpensive protection is the underlying and rising price of care. Sadly, expertise means that increasing HSAs won’t sort out this downside or meaningfully increase protection. The lack of federal income related to HSAs’ regressive tax cuts might thwart insurance policies that increase well being care entry for individuals with the best want—those that are presently least more likely to have entry to inexpensive protection and care.

*Creator’s be aware: this weblog was up to date on April 16, 2024 so as to add details about the share of individuals with personal insurance coverage who’ve HSAs and so as to add clarifying language regarding the income affect of proposed federal laws.