Fiduciary legal responsibility insurance coverage is without doubt one of the least understood insurance policies however for those who deal with advantages plans, this protection can show useful. Learn how it really works

Fiduciary legal responsibility insurance coverage, also referred to as administration legal responsibility insurance coverage, is meant to guard companies and employers towards claims ensuing from a breach in fiduciary responsibility. Primarily, the coverage protects events towards legal responsibility for managing or administering worker advantages plans.

On this article, Insurance coverage Enterprise solutions all of the urgent questions on one of many least understood insurance coverage insurance policies on the market. If your online business handles worker advantages plans and also you need to be taught extra about this often-complex type of protection, this information may help you sift via the jargon. Learn on and discover out all the pieces it’s worthwhile to find out about fiduciary legal responsibility insurance coverage.

Underneath the Worker Retirement Revenue Safety Act of 1974 (ERISA), each particular person included in an worker profit plan doc by title or title might be thought of a fiduciary. This contains anybody with discretionary decision-making authority over the administration or administration of the plan or its belongings.

Widespread fiduciaries embody:

- Employers (who’re sometimes the plan sponsors)

- Plan directors

- Plan trustees

- Administrators and officers

- Inner funding committees

“As a fiduciary, it’s your job to pick out advisors and investments, decrease bills and comply with plan paperwork precisely,” business P&C insurance coverage big Vacationers explains in its fiduciary legal responsibility insurance coverage primer. “You will have an obligation to behave solely within the curiosity of plan contributors and beneficiaries – not the corporate. That’s loads of duty and it comes with potential legal responsibility that requires the best safety.”

A fiduciary works within the curiosity of a beneficiary, particularly when an worker advantages plan underneath ERISA is concerned. A fiduciary has the responsibility of appearing within the curiosity of a principal or beneficiary. The fiduciary’s position is to supply their beneficiaries with some monetary profit.

The beneficiary, in the meantime, is the individual or entity named in an worker advantages plan. Because the title suggests, they’re those who’re set to learn or obtain compensation underneath the plan.

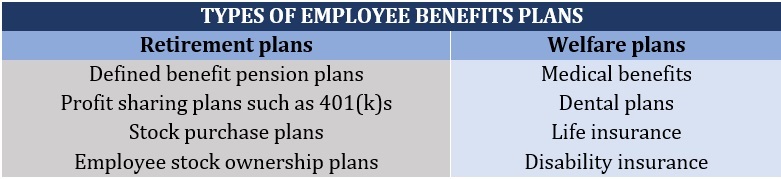

Worker advantages plans, that are managed and administered by fiduciaries, fall into two broad classes:

- Retirements plans

- Welfare plans

The desk under lists some examples underneath most of these plans.

Life insurance coverage is without doubt one of the hottest varieties of worker advantages plans. Be taught extra about how life insurance coverage works on this complete information.

ERISA was handed in 1974 to make sure that workers collaborating in profit plans, whether or not pension plans or welfare plans, get the advantages promised by such choices. The legislation doesn’t require employers to arrange these plans for employees. Slightly, it polices the plans as soon as they’re put in place to make sure they meet sure requirements.

The introduction of ERISA basically created fiduciary legal responsibility exposures for employers that supply worker advantages plans. On account of this, fiduciary legal responsibility insurance coverage grew to become extensively out there within the mid-Nineteen Seventies.

Any advantages plan coated by ERISA requires fiduciaries or trustees to behave completely within the curiosity of workers collaborating in the advantages plan, and their beneficiaries.

Different duties embody:

- Performing duties with prudence

- Adhering to the plan paperwork

- Diversifying investments

- Paying cheap bills for managing the plan

Fiduciary legal responsibility insurance coverage will solely cowl the insured firm and its workers engaged in fiduciary roles. The protection doesn’t prolong to 3rd events, outdoors advisers, or directors of advantages plans.

“Any outdoors advisers, consultants, or directors of your advantages plans … are chargeable for securing their very own protection,” explains P&C and group advantages insurer The Hartford in its enterprise proprietor’s playbook. “Additionally, understand that even for those who rent outdoors advisors to take in your plans’ fiduciary features, this doesn’t routinely exclude you from any related liabilities. You might be nonetheless chargeable for monitoring these fiduciaries’ actions.”

Fiduciary legal responsibility insurance coverage protects fiduciaries towards claims alleging:

- Errors in administering plans, similar to improper enrolment or terminations, leading to misplaced or incorrect advantages

- Errors in counseling when administering well being or welfare plans, leading to misplaced or incorrect advantages

- Giving poor or negligent recommendation on investing workers’ retirement plans

- Making dangerous investments in an outlined profit pension plan

- Wrongful denial or improper change in advantages

- Imprudent choice of and/or monitoring of third-party service suppliers

Fiduciary legal responsibility insurance coverage protection works nearly the identical as skilled legal responsibility insurance coverage, which known as errors and omissions (E&O) insurance coverage in sure industries.

Fiduciary legal responsibility insurance coverage doesn’t cowl a fiduciary who deliberately commits fraudulent acts. These embody crimes that have an effect on the advantages plan. Crimes are merely not coated by this sort of insurance coverage.

Other than crimes like fraud, embezzlement, or theft, fiduciary legal responsibility protection doesn’t cowl mismanagement or failure to fund a advantages plan.

The sort of insurance coverage coverage likewise doesn’t cowl third-party fiduciary service suppliers within the occasion they mismanage the plan.

Any firm that provides advantages plans has this publicity. Whereas massive organizations usually tend to have skilled personnel devoted to worker advantages and well-versed in ERISA legislation, smaller corporations might not. Due to this fact, smaller companies may be extra prone to litigation.

Among the many many types of legal responsibility insurance coverage that an organization can have, only a few are legally required. Fiduciary legal responsibility insurance coverage is a type of not required by legislation.

Whereas not obligatory, this sort of insurance coverage might be very helpful, particularly if a enterprise decides to have or already has some type of advantages plan in place for his or her workers.

No, it’s not. Worker advantages legal responsibility insurance coverage offers protection for worker plan claims, however is restricted to administrative errors, like failure to enroll. It doesn’t prolong to breaches of fiduciary responsibility similar to imprudent funding and so forth. This protection is generally an endorsement to a normal legal responsibility coverage.

Opposite to in style perception, ERISA bonds, worker advantages legal responsibility insurance coverage, and to some extent administrators’ and officers’ (D&O) insurance coverage won’t totally cowl fiduciary exposures. That’s why fiduciary legal responsibility insurance coverage performs a novel and very important position.

What’s fiduciary legal responsibility insurance coverage and why it is necessary on your plan. #Fiduciaryhttps://t.co/4iAcgijNIA

— EPIC Retirement Plan Companies (@epic_rps) October 13, 2023

ERISA bonds are required underneath part 412(a) of the ERISA legislation. They’re totally different from fiduciary legal responsibility insurance coverage.

This primary-party protection protects the plan and its contributors by bonding any worker who handles funds or some other property of the plan. This protects the plan from danger of loss from fraud or dishonesty by the bonded workers.

Whereas each varieties of insurance coverage are involved with retirement, advantages, or a well being plan, their major distinction lies during which celebration is roofed.

ERISA legal responsibility insurance coverage protects an worker advantages plan and its contributors.

Fiduciary legal responsibility insurance coverage, in the meantime, protects corporations from legal responsibility whereas serving because the fiduciary or trustee of an worker advantages plan.

For instance, if a enterprise proprietor and their firm put up a advantages plan for his or her workers, the enterprise proprietor is taken into account a fiduciary. They have to fulfill their fiduciary duties as set by the US Division of Labor.

The enterprise proprietor and sure workers are thought of fiduciaries if they’ve authority over, advise, handle, or administer the plan.

Fiduciary legal responsibility insurance coverage covers the fiduciaries and may cowl claims arising from:

- Errors when administering advantages

- Irresponsible or negligent funding practices

- Wrongful denial of advantages to a plan participant

- Losses ensuing from failure to handle third celebration service suppliers

ERISA legal responsibility insurance coverage covers the advantages plan and its contributors.

Usually, this type of protection requires that any worker who handles funds or different property hooked up to the advantages plan be bonded.

The bond that’s used makes the fiduciaries personally liable, theoretically defending the plan from danger of loss on account of fraud or dishonesty on their half.

The kind of bond that ERISA legal responsibility prescribes is a constancy bond. Constancy bonds are used to make sure that these bonded don’t incur losses from mismanagement, dishonesty, or acts of fraud.

A constancy bond is restricted to a person. A surety bond, alternatively, is restricted to performing a job or executing a activity, together with fulfilling a contractual obligation and cost.

Merely put, a constancy bond ensures or covers an individual whereas a surety bond ensures efficiency.

No. Fiduciary legal responsibility insurance coverage offers protection for danger or loss ensuing from negligence, mismanagement, or errors. Intentional acts like fraud or theft inflicting loss to a advantages plan or its belongings aren’t coated; that’s the area of a selected crime protection coverage.

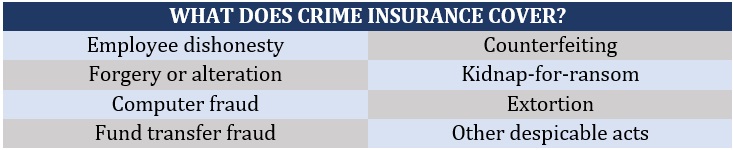

Crime protection is an insurance coverage coverage towards loss attributable to fraudulent or willful felony acts. The desk under lists some examples of crimes coated underneath this sort of coverage.

Crime insurance policies can cowl a variety of crimes dedicated by each workers and outsiders.

Sure. There are some insurance coverage corporations that supply crime protection particularly for small and medium-sized companies to mitigate danger or loss on account of fraudulent acts.

- Forgery

- Worker dishonesty and its ensuing property loss

- Pc fraud

- Fund switch fraud

- Forex and securities theft

Losses ensuing from social engineering are additionally included and may include a protection of no less than $100,000.

With the fast shift to digital transformation, the insurance coverage business has additionally seen an upsurge in digital crimes. You’ll be able to take a look at our cyber crime report tracker for the most recent information breach and different cyber incidents involving insurance coverage corporations. Make sure you bookmark this web page as it’s up to date usually.

Sure. Fiduciary legal responsibility insurance coverage is a superb type of danger administration. It protects the pursuits of your organization and your workers. It’s designed to guard a enterprise from claims arising from mismanagement and legal responsibility from fiduciaries, similar to errors and miscarriage of fiduciary duties.

Fiduciary legal responsibility insurance coverage may defend each the corporate and workers from fiduciary-related negligence, mismanagement, or any acts that may hurt the plan contributors.

That largely relies on whether or not your organization presents any type of worker advantages plan. If your organization is so small that it merely can’t afford to supply any advantages packages, then a fiduciary insurance coverage coverage shouldn’t be obligatory.

As soon as your organization grows and decides to supply any kind of worker advantages, that’s when getting fiduciary legal responsibility insurance coverage turns into a sound concept.

Though fiduciary legal responsibility insurance coverage isn’t legally required when an organization has a advantages plan, ERISA legal responsibility insurance coverage is legally required by US labor legal guidelines.

Is fiduciary legal responsibility insurance coverage a worthwhile funding? Do you might have an expertise the place this sort of protection helped? We’d like to see your story within the feedback part under.

Associated Tales

Sustain with the most recent information and occasions

Be a part of our mailing listing, it’s free!